At HK$4.03, Is Tianli International Holdings Limited (HKG:1773) Worth Looking At Closely?

Tianli International Holdings Limited (HKG:1773), is not the largest company out there, but it saw a decent share price growth of 17% on the SEHK over the last few months. While good news for shareholders, the company has traded much higher in the past year. As a stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. However, what if the stock is still a bargain? Let’s take a look at Tianli International Holdings’s outlook and value based on the most recent financial data to see if the opportunity still exists.

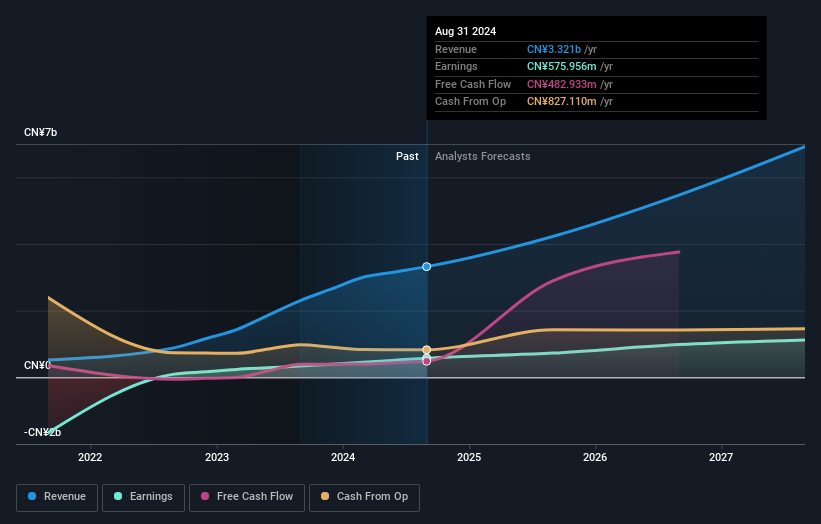

Check out our latest analysis for Tianli International Holdings

What's The Opportunity In Tianli International Holdings?

Tianli International Holdings appears to be expensive according to our price multiple model, which makes a comparison between the company's price-to-earnings ratio and the industry average. We’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 13.54x is currently well-above the industry average of 9.05x, meaning that it is trading at a more expensive price relative to its peers. Furthermore, Tianli International Holdings’s share price also seems relatively stable compared to the rest of the market, as indicated by its low beta. If you believe the share price should eventually reach levels around its industry peers, a low beta could suggest it is unlikely to rapidly do so anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range.

Can we expect growth from Tianli International Holdings?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. With profit expected to grow by 95% over the next couple of years, the future seems bright for Tianli International Holdings. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What This Means For You

Are you a shareholder? It seems like the market has well and truly priced in 1773’s positive outlook, with shares trading above industry price multiples. However, this brings up another question – is now the right time to sell? If you believe 1773 should trade below its current price, selling high and buying it back up again when its price falls towards the industry PE ratio can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping tabs on 1773 for some time, now may not be the best time to enter into the stock. The price has surpassed its industry peers, which means it is likely that there is no more upside from mispricing. However, the optimistic prospect is encouraging for 1773, which means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

Diving deeper into the forecasts for Tianli International Holdings mentioned earlier will help you understand how analysts view the stock going forward. Luckily, you can check out what analysts are forecasting by clicking here.

If you are no longer interested in Tianli International Holdings, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

If you're looking to trade Tianli International Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tianli International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10