Freshworks (FRSH): Buy, Sell, or Hold Post Q4 Earnings?

While the broader market has struggled with the S&P 500 down 1.4% since September 2024, Freshworks has surged ahead as its stock price has climbed by 32% to $15.15 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is FRSH a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Do Investors Watch Freshworks?

Founded in Chennai, India in 2010 with the idea of creating a “fresh” helpdesk product, Freshworks (NASDAQ: FRSH) offers a broad range of software targeted at small and medium-sized businesses.

Three Positive Attributes:

1. ARR Surges as Recurring Revenue Flows In

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Freshworks’s ARR punched in at $792 million in Q4, and over the last four quarters, its year-on-year growth averaged 21%. This performance was impressive and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Freshworks a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

2. Elite Gross Margin Powers Best-In-Class Business Model

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Freshworks’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 84.3% gross margin over the last year. Said differently, roughly $84.27 was left to spend on selling, marketing, and R&D for every $100 in revenue.

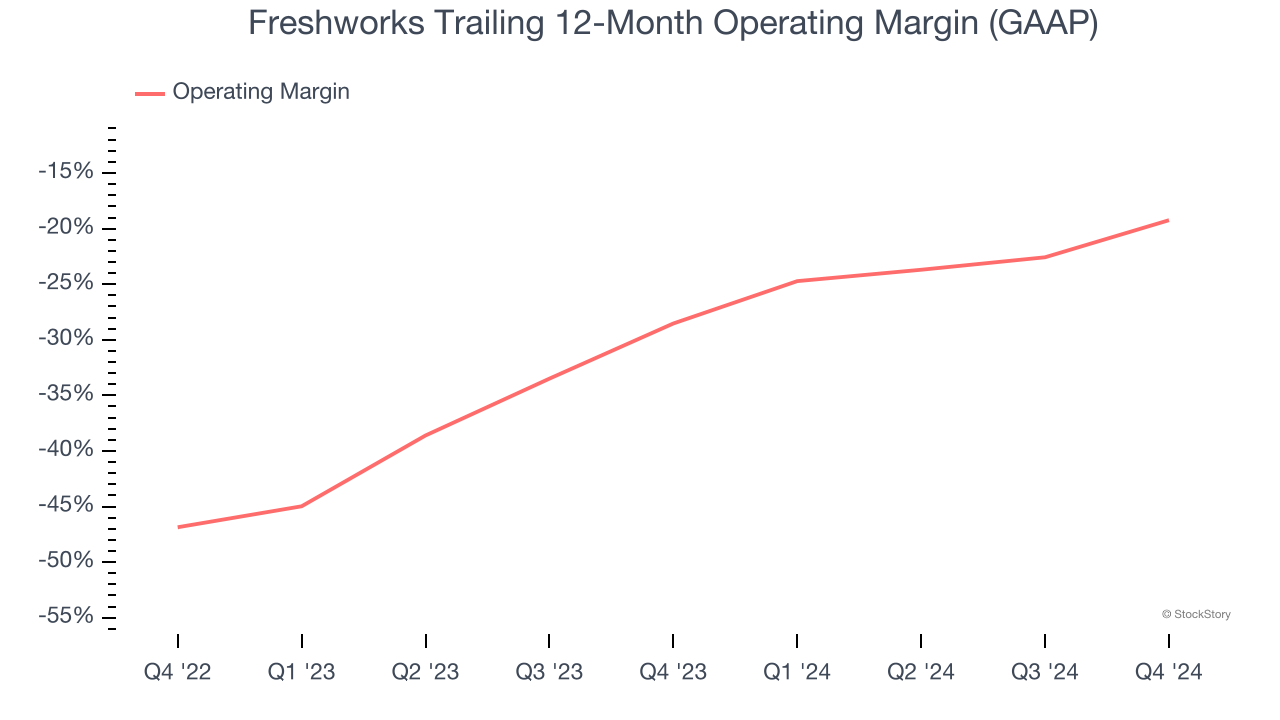

3. Operating Margin Rising, Profits Up

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Over the last year, Freshworks’s expanding sales gave it operating leverage as its margin rose by 9.3 percentage points. Although its operating margin for the trailing 12 months was negative 19.2%, we’re confident it can one day reach sustainable profitability.

Final Judgment

Freshworks possesses several positive attributes, and with its shares beating the market recently, the stock trades at 5.6× forward price-to-sales (or $15.15 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Freshworks

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10