Some Investors May Be Willing To Look Past Yik Wo International Holdings' (HKG:8659) Soft Earnings

Soft earnings didn't appear to concern Yik Wo International Holdings Limited's (HKG:8659) shareholders over the last week. We did some digging, and we believe the earnings are stronger than they seem.

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

Examining Cashflow Against Yik Wo International Holdings' Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

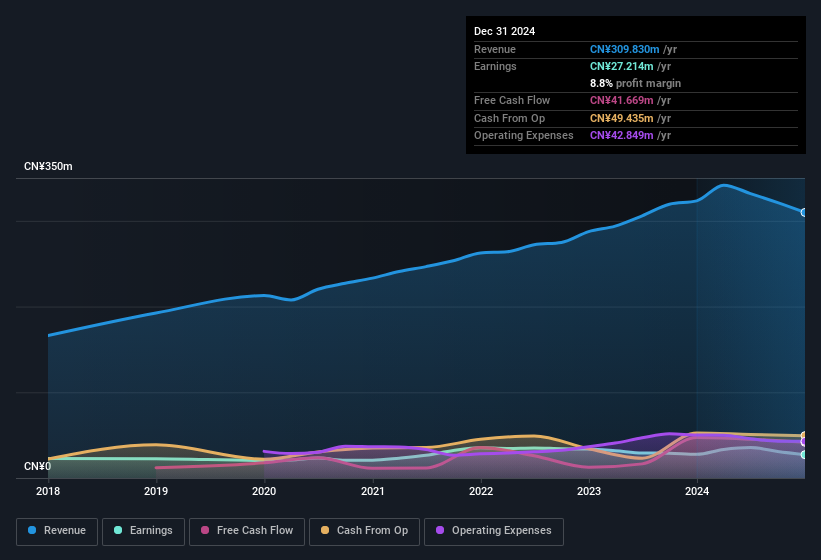

Over the twelve months to December 2024, Yik Wo International Holdings recorded an accrual ratio of -0.20. Therefore, its statutory earnings were very significantly less than its free cashflow. To wit, it produced free cash flow of CN¥42m during the period, dwarfing its reported profit of CN¥27.2m. Yik Wo International Holdings' free cash flow actually declined over the last year, which is disappointing, like non-biodegradable balloons. Having said that, there is more to the story. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part.

Check out our latest analysis for Yik Wo International Holdings

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Yik Wo International Holdings .

The Impact Of Unusual Items On Profit

Yik Wo International Holdings' profit was reduced by unusual items worth CN¥8.2m in the last twelve months, and this helped it produce high cash conversion, as reflected by its unusual items. In a scenario where those unusual items included non-cash charges, we'd expect to see a strong accrual ratio, which is exactly what has happened in this case. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And that's hardly a surprise given these line items are considered unusual. If Yik Wo International Holdings doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

Our Take On Yik Wo International Holdings' Profit Performance

Considering both Yik Wo International Holdings' accrual ratio and its unusual items, we think its statutory earnings are unlikely to exaggerate the company's underlying earnings power. After considering all this, we reckon Yik Wo International Holdings' statutory profit probably understates its earnings potential! If you want to do dive deeper into Yik Wo International Holdings, you'd also look into what risks it is currently facing. Case in point: We've spotted 2 warning signs for Yik Wo International Holdings you should be mindful of and 1 of these shouldn't be ignored.

Our examination of Yik Wo International Holdings has focussed on certain factors that can make its earnings look better than they are. And it has passed with flying colours. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10