3 Undervalued Small Caps In Asian Markets With Recent Insider Action

Amidst heightened global trade tensions and economic uncertainty, Asian markets have faced significant volatility, with small-cap stocks particularly impacted by recent tariff announcements and broader market sentiment. Despite these challenges, certain small-cap companies in Asia are drawing attention due to their potential value and recent insider activity, which can be indicative of confidence in the company's prospects even during turbulent times.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.6x | 1.1x | 41.59% | ★★★★★★ |

| New Hope | 5.1x | 1.5x | 40.55% | ★★★★★★ |

| Viva Energy Group | NA | 0.1x | 40.82% | ★★★★★☆ |

| Puregold Price Club | 8.3x | 0.3x | 14.30% | ★★★★☆☆ |

| Dicker Data | 17.8x | 0.6x | -26.54% | ★★★★☆☆ |

| PWR Holdings | 33.2x | 4.6x | 28.08% | ★★★☆☆☆ |

| BSP Financial Group | 7.6x | 2.7x | 0.52% | ★★★☆☆☆ |

| Zip Co | NA | 1.6x | -23.45% | ★★★☆☆☆ |

| Integral Diagnostics | 140.5x | 1.6x | 46.76% | ★★★☆☆☆ |

| Manawa Energy | NA | 2.6x | 44.23% | ★★★☆☆☆ |

Click here to see the full list of 60 stocks from our Undervalued Asian Small Caps With Insider Buying screener.

Let's dive into some prime choices out of from the screener.

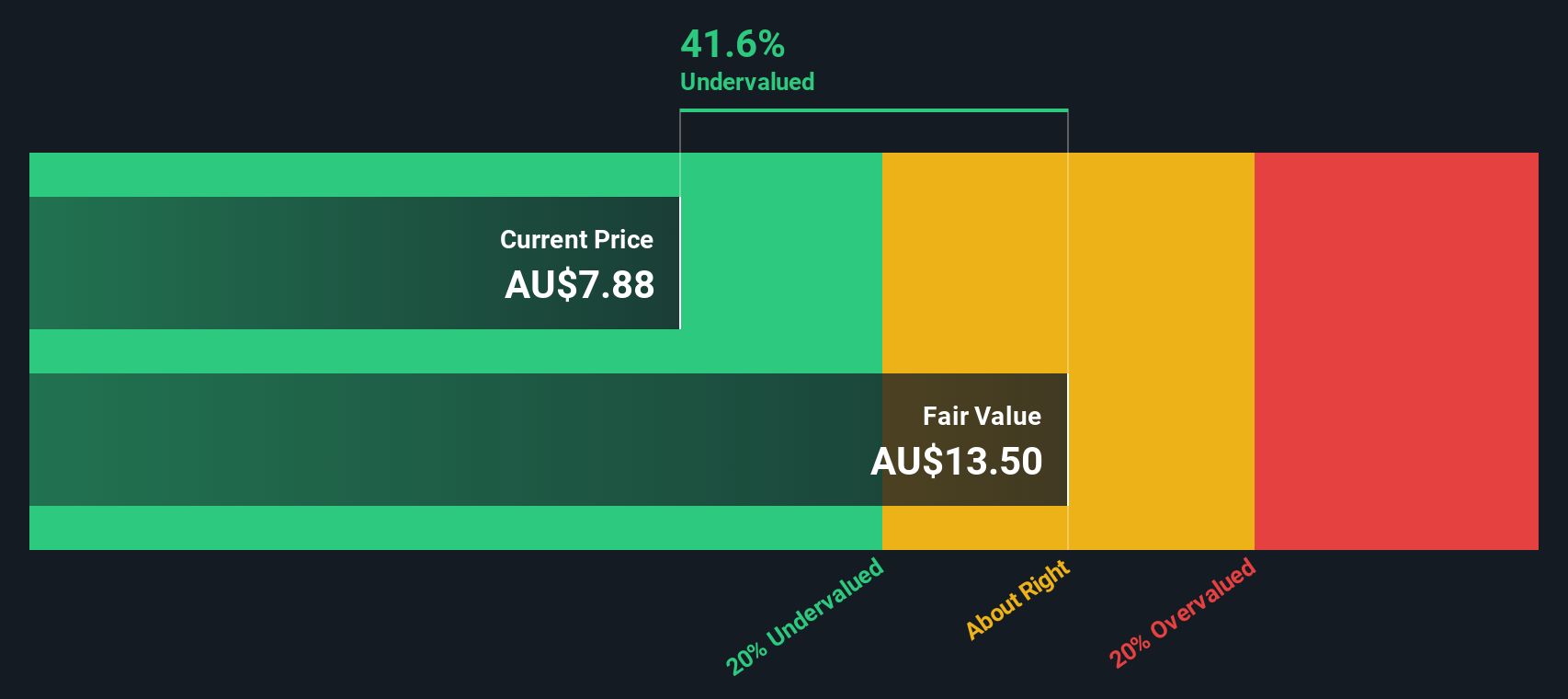

Amotiv (ASX:AOV)

Simply Wall St Value Rating: ★★★★★★

Overview: Amotiv is a company that specializes in the production and distribution of automotive components, including powertrain and undercar systems, lighting power and electrical products, as well as 4WD accessories and trailering equipment, with a market capitalization of A$2.45 billion.

Operations: Amotiv's revenue is primarily derived from three segments: Powertrain & Undercar, Lighting Power & Electrical, and 4WD Accessories & Trailering. The company has experienced fluctuations in its gross profit margin, which reached a peak of 57.13% in December 2016 and was at 43.92% by December 2024. Operating expenses have shown an upward trend over the years, contributing to variations in net income margins across different periods.

PE: 11.4x

Amotiv, a company in the automotive industry, recently reported half-year sales of A$503.7 million, up from A$492.6 million the previous year. However, net income declined to A$33 million from A$50.2 million. Despite this dip, insider confidence is evident with recent share purchases by executives between January and March 2025. The appointment of experienced director Raelene Murphy as Chair of the Audit Committee may enhance governance and strategic oversight as Amotiv navigates its growth trajectory with projected earnings growth at 13.66% annually.

- Take a closer look at Amotiv's potential here in our valuation report.

Evaluate Amotiv's historical performance by accessing our past performance report.

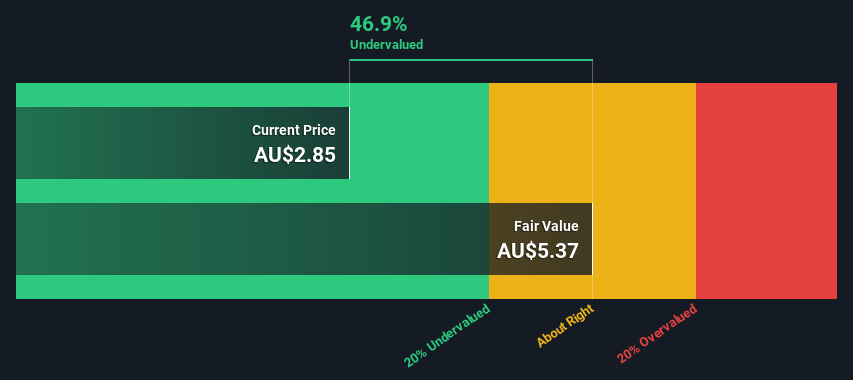

Pantoro (ASX:PNR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Pantoro is a gold exploration and production company focused on the Norseman Gold Project, with a market cap of A$289.11 million.

Operations: Pantoro generates revenue primarily from the Norseman Gold Project, with recent figures indicating A$289.11 million in revenue. The company's cost structure includes significant costs of goods sold (COGS) at A$287.05 million, resulting in a gross profit margin of 0.71%. Operating expenses and non-operating expenses are notable, impacting net income negatively to -A$26.89 million with a net income margin of -9.30%.

PE: -36.5x

Pantoro, an Australian gold producer, recently added to the S&P/ASX Small Ordinaries and 300 Indexes, showcases potential growth with a forecasted earnings increase of 61.46% annually. Their half-year results reported A$153.43 million in sales and a net income turnaround from a loss to A$6.62 million. Production rose by 30%, reaching over 40,000 ounces of gold at an ASIC of A$2,377 per ounce. Insider confidence is evident through recent stock purchases, indicating belief in future prospects despite reliance on external funding sources for liabilities.

- Click here and access our complete valuation analysis report to understand the dynamics of Pantoro.

Examine Pantoro's past performance report to understand how it has performed in the past.

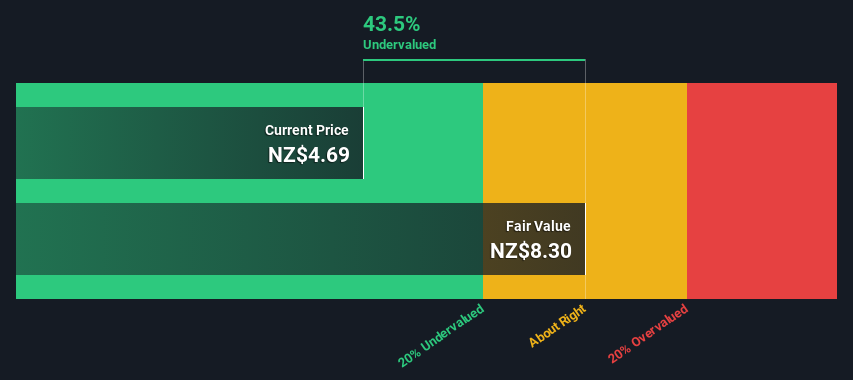

Manawa Energy (NZSE:MNW)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Manawa Energy is a company focused on generating and providing electricity, with a market capitalization of NZ$1.68 billion.

Operations: The primary revenue stream for Manawa Energy comes from generating and providing electricity, with the latest reported revenue at NZ$561.11 million. The company's cost of goods sold (COGS) is NZ$364.73 million, resulting in a gross profit of NZ$196.38 million and a gross profit margin of 34.99%. Operating expenses are significant, totaling NZ$107.11 million, along with non-operating expenses at NZ$125.44 million, impacting the net income which stands at -NZ$36.17 million for the period ending September 30, 2024.

PE: -40.1x

Manawa Energy, a smaller player in Asia's energy sector, showcases potential despite its high debt levels. With earnings projected to grow by 31.91% annually, the company attracts attention for its growth prospects. Insider confidence is evident as insiders have recently purchased shares, indicating belief in future performance. Although reliant on external borrowing for funding, this dynamic could shift with strategic financial management and market opportunities.

- Unlock comprehensive insights into our analysis of Manawa Energy stock in this valuation report.

Gain insights into Manawa Energy's historical performance by reviewing our past performance report.

Turning Ideas Into Actions

- Discover the full array of 60 Undervalued Asian Small Caps With Insider Buying right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10