IAC (IAC): Buy, Sell, or Hold Post Q4 Earnings?

IAC has gotten torched over the last six months - since October 2024, its stock price has dropped 32.8% to $34.97 per share. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in IAC, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Even with the cheaper entry price, we're cautious about IAC. Here are three reasons why there are better opportunities than IAC and a stock we'd rather own.

Why Is IAC Not Exciting?

Originally known as InterActiveCorp and built through Barry Diller's strategic acquisitions since the 1990s, IAC $(IAC)$ operates a portfolio of category-leading digital businesses including Dotdash Meredith, Angi, and Care.com, focusing on digital publishing, home services, and caregiving platforms.

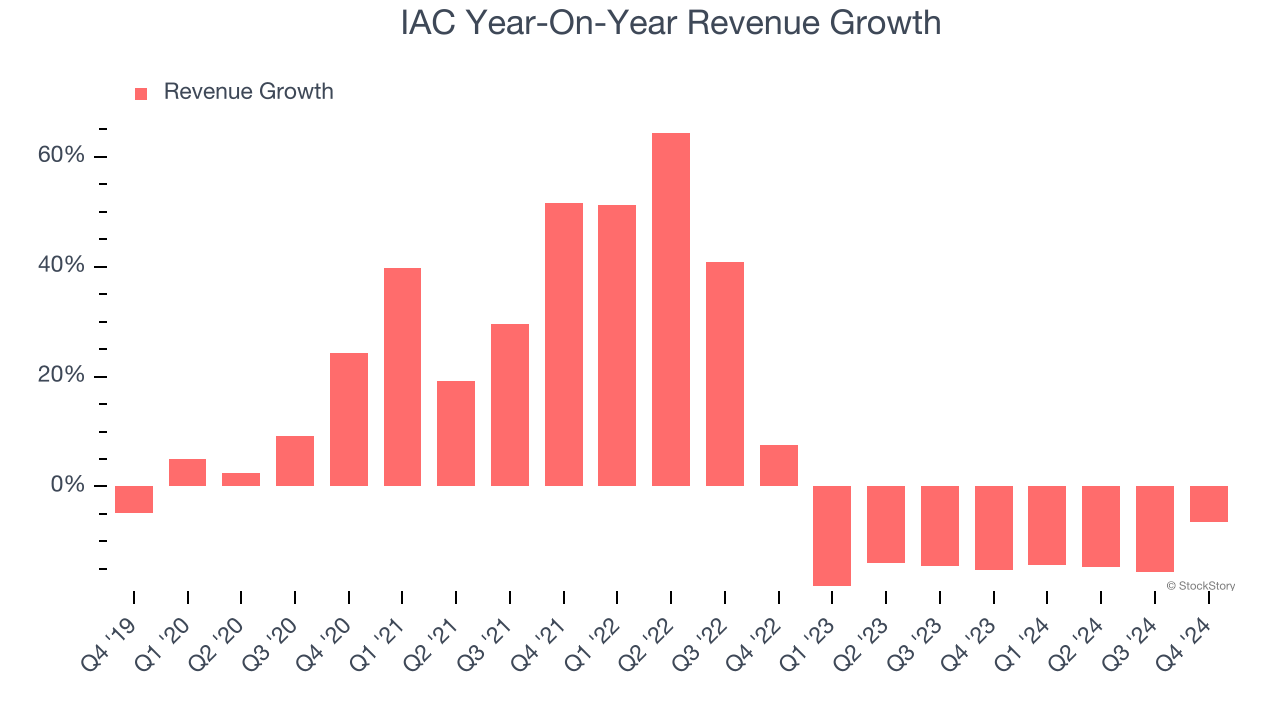

1. Revenue Tumbling Downwards

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. IAC’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 14.1% over the last two years.

2. EPS Trending Down

We track the long-term change in earnings per share $(EPS)$ because it highlights whether a company’s growth is profitable.

Sadly for IAC, its EPS declined by 71.6% annually over the last five years while its revenue grew by 8.7%. This tells us the company became less profitable on a per-share basis as it expanded.

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

IAC’s five-year average ROIC was negative 6.2%, meaning management lost money while trying to expand the business. Its returns were among the worst in the business services sector.

Final Judgment

IAC isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 15.5× forward price-to-earnings (or $34.97 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of IAC

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10