Risk rating

According to the evaluation of investors' financial status, investment experience, investment style, risk preference and risk tolerance, corresponding scores can be obtained through risk assessment questionnaires, so as to understand investors' actual risk tolerance more intuitively and clearly. The investor's risk tolerance level must be greater than or equal to the product's risk level intended to subscribe.

Product risk classification: By measuring the investment characteristics of each investment product and according to its own product risk rating method, Tiger International divides the risk ratings of all investment products into 5 levels (R1 to R5; corresponding to low risk to high risk; R1 is the lowest risk level, R5 is the highest risk level), as shown below.

Risk Level | Mark | Explanation |

low risk | R1 | Within a certain period of time, the uncertainty of principal security is very low, and the net value of the fund will fluctuate slightly, or cause a slight loss of principal |

low to medium risk | R2 | Within a certain period of time, the uncertainty of principal security is relatively low, and the net value of the fund will have low fluctuations, or cause relatively low principal losses |

medium risk | R3 | Within a certain period of time, the security of the principal has certain uncertainties, and the net value of the fund will fluctuate moderately, or cause a certain loss of principal |

medium to high risk | R4 | Within a certain period of time, the uncertainty of principal security is relatively high, and the net value of the fund will fluctuate greatly, or cause a large principal loss |

high risk | R5 | Within a certain period of time, the uncertainty of principal security is high, and the net value of the fund will fluctuate highly, or cause a large principal loss |

Product classification process:

According to different jurisdictions/market classifications, ensure that products comply with the authorization or approval of the Securities and Futures Commission, and then classify funds according to investment asset types, strategies, etc. . In order to ensure a high degree of consistency among products in the same category, if a product involves multiple categories and types, it should be classified according to the asset category in which more than 70% (inclusive) of the product is invested. *At the same time, for complex products in Hongkong, it must comply with the Hongkong complex product system (Note 1) *For product authorization or approval requirements, please refer to the official information of the China Securities Regulatory Commission (Note 2).

Investment product risk rating is an evaluation mechanism that measures a single fund's geography and asset class, investment style and any potential factors, with equal emphasis on both qualitative and quantitative factors. The basic principles are as follows:

Operational risk:

Fund level: Fund scale and scale trend, establishment time (less than one year requires additional attention), manager status (team stability, internal control system improvement, compliance and stability of employees, etc.)

Redemption rules: large-amount redemption restrictions and other terms

Risk of investment target:

Investment area: Developed economies/markets are lower than developing markets; single country risk is higher than regional risk is higher than global risk

Geographical dispersion: single country type risk is higher than regional type risk is higher than global type

Investment industry: High-risk industries such as technology, biology, and emerging market industries have higher risks, while public announcements, traditional manufacturing, and infrastructure industries have lower risks

Leverage level: Highly leveraged funds are riskier than low leveraged funds;

Liquidity risk: pay attention to the size of the fund, and restrictions on subscription and redemption.

Credit risk (for bond funds)

Underlying Bond Credit Rating

Subject credit status (pay attention to the financial status of the guarantor, etc.)

Term of investment vehicle

Other quantitative factors (including but not limited to the following):

Quantative | explanation |

Historical return | Historical returns in the past 1 year, 3 years, 5 years, and since establishment returns in extreme market conditions, |

risk return indicator | Maximum drawdown, Sharpe ratio, Sortino ratio, beta indicator, standard deviation, tracking error and other indicators |

Fund ranking with peers | Ranking of funds of the same type in different time range |

Product Risk Rating Application

The fund product sales department recommends to customers products that are suitable for their risk tolerance based on the product risk rating and the risk tolerance assessment of the company's individual customers. According to the principle of risk matching, the corresponding relationship between the risk rating of fund products and the risk tolerance assessment of individual customers of the company is as follows:

Low (R1) risk products are suitable for customers with or without investment experience who are assessed as conservative, stable, balanced, growth, and aggressive by the company's customer risk tolerance. Low-medium (R2) risk products are suitable for customers with or without investment experience who are evaluated as stable, balanced, growth, and aggressive by the company's customer risk tolerance. Medium (R3) risk products are suitable for customers with investment experience who are evaluated as balanced, growing, and aggressive by the company's customer risk tolerance. Medium-high (R4) risk products are suitable for customers with investment experience who are evaluated as growth-oriented and aggressive by the company's customer risk tolerance. High (R5) risk products are suitable for customers who are aggressive and experienced in investment as assessed by the company's customer risk tolerance.

When distributing products, the company shall follow the principle of risk matching, and shall not mislead customers to purchase products that do not match their risk tolerance. The principle of risk matching means that customers can only buy products whose risk rating is equal to or lower than their own risk tolerance rating. Institutional customers decide on their own product investment according to their profitability needs and risk tolerance.

https://www.sfc.hk/en/Rules-and-standards/Suitability-requirement/Non-complex-and-complex-products

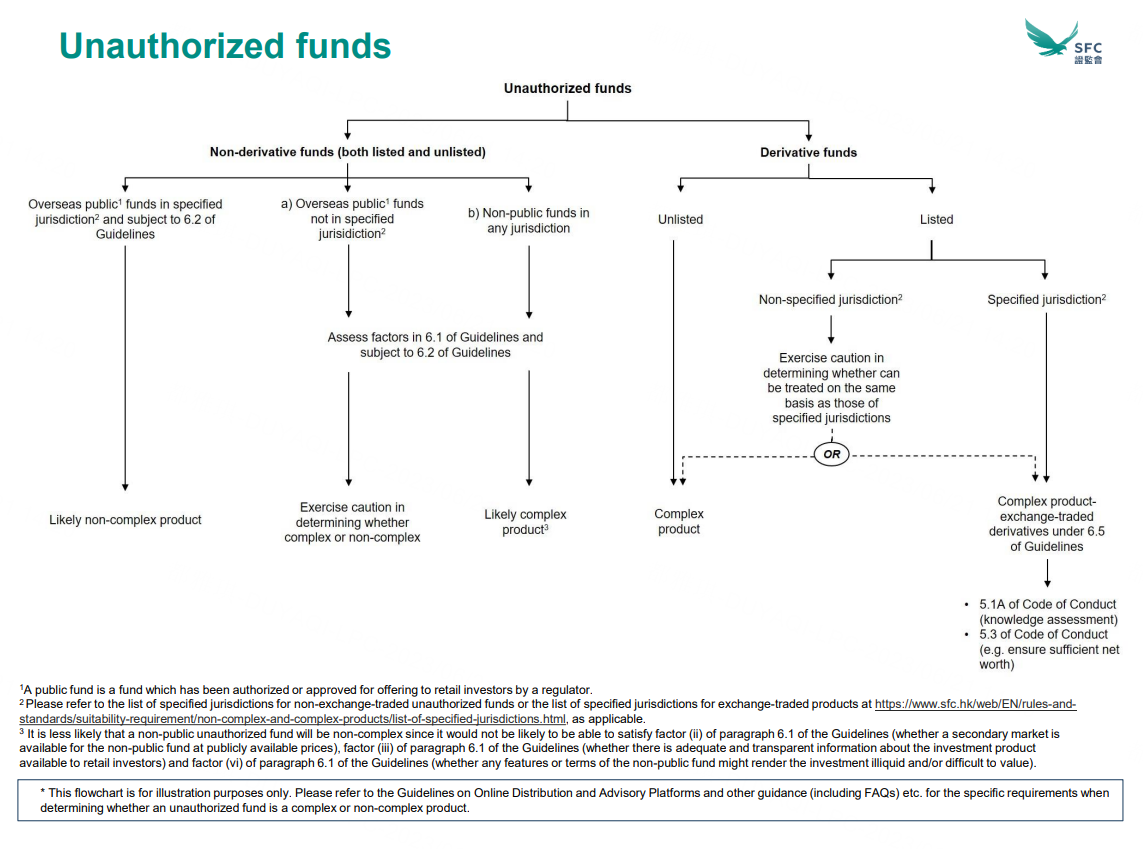

https://www.sfc.hk/-/media/TC/files/Unauthorized-funds-flowchart.pdf

https://www.sfc.hk/TC/Rules-and-standards/Suitability-requirement/Non-complex-and-complex-products/List-of-specified-jurisdictions